On November 3, 2023, Citizens Bank collapsed.

Its closure marked the fifth US bank failure of 2023, the most bank failures in a single year since 2017.

After a few years of calm, people in the US rediscovered a hard truth:

Even the safest assets and most trustworthy institutions can fail.

Risk abounds — sometimes, in the most unlikely places, like US treasuries or auto loans.

In the spring, it was Credit Suisse. In the fall, it was China. Next year, maybe it’ll be CLOs or commercial real estate.

What about Japanese bonds? Canadian mortgages? A collapsing ruble? A global recession? A new war?

With every crisis, the “macro” looks worse.

Face the music

Yet, we still have money. What shall we do with it?

For more than a year, I’ve split money into cash, crypto, and bonds (specifically, t-bills). No matter what happens to the US economy, I’m covered.

The New 60/40 Portfolio: Bonds, Bitcoin, and Cash?

So far, the bonds have returned about 5% on average. Bitcoin’s up about 80% over that time. I used the cash to pay down lines of credit at 7-8% annual interest.

Meanwhile, the S&P 500 is up 3% and the TLT is down 7% over that time.

I must sound like a pretty smart guy, right?

Hardly. I’m a crypto guy. What the hell do I know about macro cycles and the implications of central bank monetary policies?

The “macro” guys say you have to follow quadrants, “don’t fight the Fed,” and worry about “draining liquidity.”

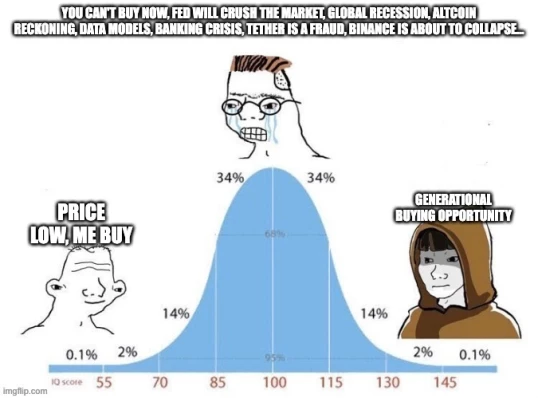

I’m not a macro guy. I saw that crypto and bonds were way below historical benchmarks. By some measures, they offer generational buying opportunities.

At the same time, US equities are still high against historical benchmarks. Bond funds will underperform until the Fed cuts rates. Real estate’s frozen (in some countries, it’s on the verge of a meltdown).

That’s a statement of today’s circumstances, not a “macro” position. The “macro” changes all the time in unpredictable ways. A recession is 100% guaranteed. Central banks will break something eventually.

The risks are real.

The timing is unclear.

As such, when an opportunity presents itself, sometimes you have to take it and hope for the best.

Uncertainty is the only certainty

People are looking for an earnings recession, a stock market crash, or at least a drop in earnings-per-share or P/E ratio back to something more in line with historical norms.

Can you trust conventional metrics like EPS and P/E? Wall Street did record amounts of buybacks in 2021 and 2022. Those buybacks artificially boosted share prices. Did those buybacks artificially elevate those metrics, too? Do these falling metrics reflect changes in how businesses reward shareholders?

Does that even matter? Most companies issue more new shares than they buy back each year. Even after the buybacks, your equity is usually getting diluted (though you benefit in other ways). This should skew the metrics in the opposite direction, right?

Does that mean EPS and P/E might actually understate the value of a stock?

Man, this stuff is confusing!

You find only what you look for

What about employment data? Are we measuring that correctly?

Since 2020, we’ve seen a boom in people using the Internet and the gig economy to make extra money on top of their day jobs. Does that skew the employment data? We’ve also seen a lot of people leave the workforce for retirement, disability, or death. Does the data properly account for that? Why do we see discrepancies between the JOBS data and the JOLTS data?

What about demographics?

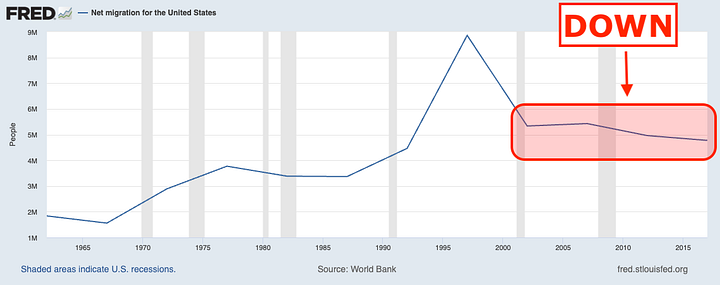

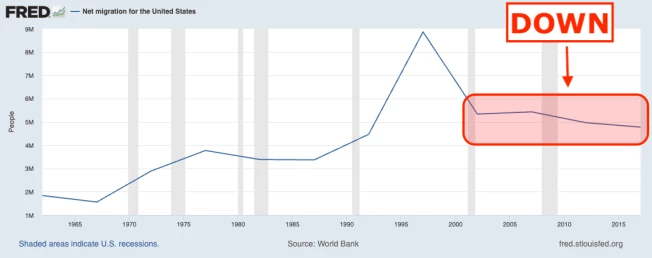

The US population is shrinking and we’re getting older, sicker, and less productive — until you include immigration.

Once you do that, US demographics look great. Our population is growing and we’re getting younger, healthier, and more productive.

But immigration’s trended down for years!

Do you include immigration in your projection because that trend might change? Or strip out immigration because it’s uncertain what will happen in the future?

What about inflation data?

At the beginning of the year, the US Bureau of Labor Statistics changed how it calculates some of the inflation metrics. What does that mean for the Fed’s analysis and their decisions? Can we still compare today’s changes with the changes that happened in the past under a different calculation?

The National Bureau of Economic Research changed its definition of recession a few years ago. Under the old definition, the US had a recession in 2022. Under the new definition, the US may never have another recession again.

No wonder it’s so hard to predict the future. We don’t even know what’s happening in the present!

Go with what you got

With all that uncertainty in the data, its construction, and its significance, how can anybody make heads or tails of anything?

The Fed says it’s going to follow the data. What does that even mean? Economics is not a science. Data only tells you one part of the story.

We will never have all the pieces of the puzzle. Only in hindsight will we know what to do, and by that time, we won’t have a chance to do anything about it.

Sure, the “macro” sucks. It always does! Priya in the Park is always telling you the market’s going to crash. She’s always right—but her timing sucks.

She’s like the boy who cried wolf. There are wolves lurking in the macro, ready to attack your sheep.

When you keep warning people about a wolf, you’d better show people a wolf. Otherwise, they’ll stop believing you. Then that day the wolf finally attacks, you’ll cry out as loud as you can and everybody else will shrug you off.

Financial hypochondriacs

For macro analysts, every negative data point is a sign of a recession. Every unhealthy shift is a new trend that will doom us.

They’re financial hypochondriacs. Every headache is a brain tumor. Every twinge is a reason to pop a pill.

For the past two years, they’ve told you to stay away from crypto. Yet, if you bought bitcoin each day for the past two years, you’d be up 17% on your investment.

(With my plan, you’re up 35% with cash to spare.)

My Plan for Buying and Selling Bitcoin

If you put the same amount into SPX each day, you’re up 4% on your investment. With cash in a money market mutual fund, you’re up 2% on your investment.

Maybe it’s not the data that’s the problem. Maybe it’s the analysts.

If that’s true, they don’t need to find better data. They need to find a psychiatrist.

That’s your advantage

The macro always sucks and nobody knows what will happen next.

Plus, your government can wave its magic wand and change everything.

Turn that uncertainty into an advantage. That uncertainty is the only reason we can take a small amount of money and turn it into an outsized stake in the financial networks of the future.

Once the “macro” is clear and people feel comfortable putting money into crypto, that opportunity will disappear. Prices will get too high. Money will get too easy. Speculative enthusiasm will replace genuine conviction.

Embrace uncertainty. Treasure doubt. Act with confidence, not in the belief in any one outcome, but in the belief that you have a sound strategy and realistic expectations.

And those other assets I talked about above?

At some point, they’ll reverse their trends. Your “macro” analyst may spot that, or maybe not.

(I won’t even try.)

Are you ready for when that time comes?

If not, get ready now.

It’s nice to have clarity about the “macro,” but it’s not necessarily the best investment strategy. You can always make up for bad timing.

Complacency kills.

This post is also available as a collectible NFT on Mirror.

Mark Helfman publishes the Crypto is Easy newsletter. He is also the author of three books and a top Bitcoin writer on Medium and Hacker Noon. Learn more about him in his bio and connect with him on Superpeer or Tealfeed.