The Fed, the US’s central bank, will soon meet to decide what to do about interest rates.

While nobody expects a rate hike, the Fed says people still have too many jobs and make too much money. It needs to “drain liquidity” and “weaken the labor market.”

Higher for longer, as it says. All in pursuit of two goals: maximum employment and stable prices.

A lot of people place a lot of faith in the Fed’s capacity to accomplish these goals.

The crypto market obsesses over the Fed’s decisions. Financial media watch it like hawks (or doves, depending on where you want interest rates to go). Huge investors plan major financial decisions around the Fed’s actions.

The economic health and vitality of the US economy hinge on its every move.

As such, you’d expect that the Fed hits its benchmarks more often than not, right? What else could validate such faith in the significance of the Fed’s actions? Its track record must justify this belief, right?

Nobody knows.

SMART goals, SHMART goals

In its Statement on Longer-Run Goals and Monetary Policy Strategy, the Fed says maximum employment is “not directly measurable and changes over time,” therefore it’s not appropriate to define a goal.

For stable prices, it sets an average of 2% inflation over time, with no standard for how to calculate that average. Does that mean 2% in a year? 2% annualized for ten years? A median of 2% over a rolling five-year period?

With no standards or benchmarks, you can’t measure the Fed’s success. But I can!

Let’s set specific, measurable, achievable, relevant, and time-bound goals, like the management and self-improvement gurus suggest.

Here goes:

- Maximum employment: an unemployment rate of 4% or less at any time. This was the layperson’s definition when I studied economics.

- Stable prices: an inflation rate of 2% or less year-over-year. This is the Fed’s stated target in its simplest form, without averages or medians.

How often does the Fed meet those goals?

Not often.

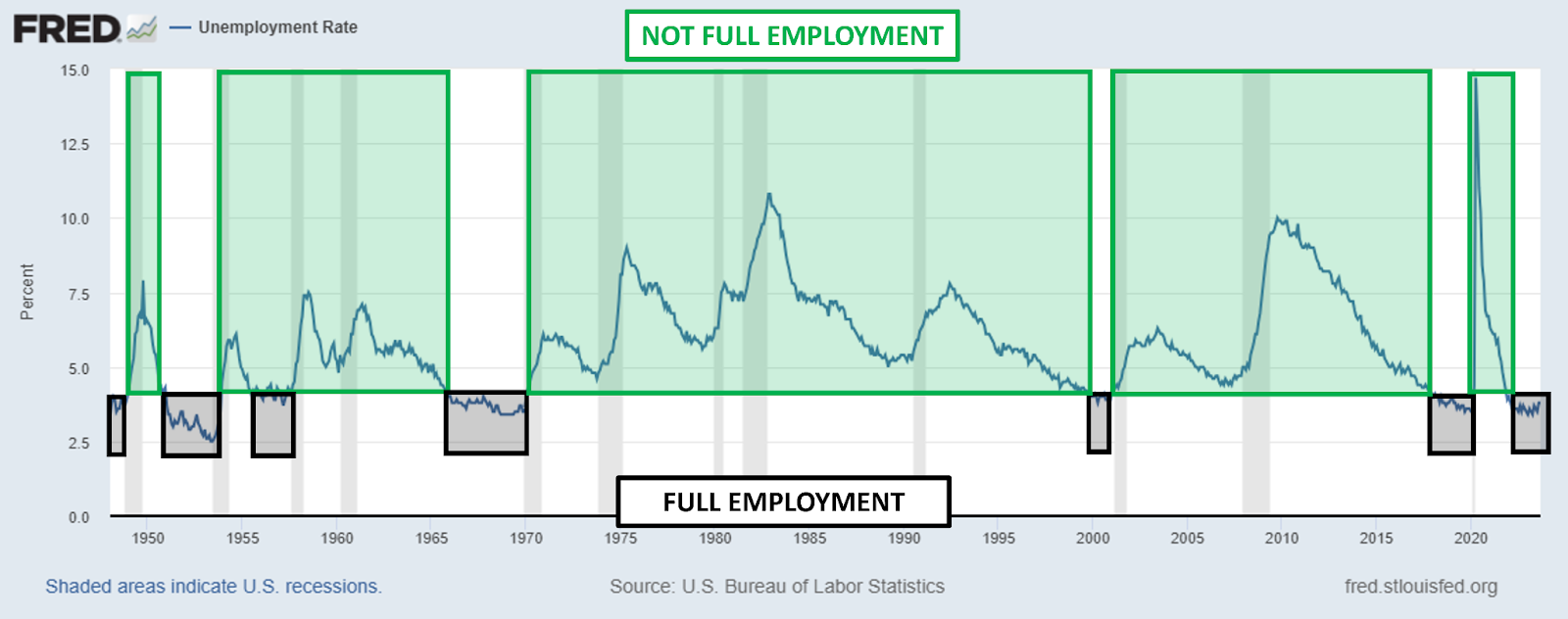

The US economy almost never reaches full employment. Look at all the “full employment” years shaded black in this image:

The unemployment rate dropped below 4% in only 162 out of 908 quarters since records started in 1948.

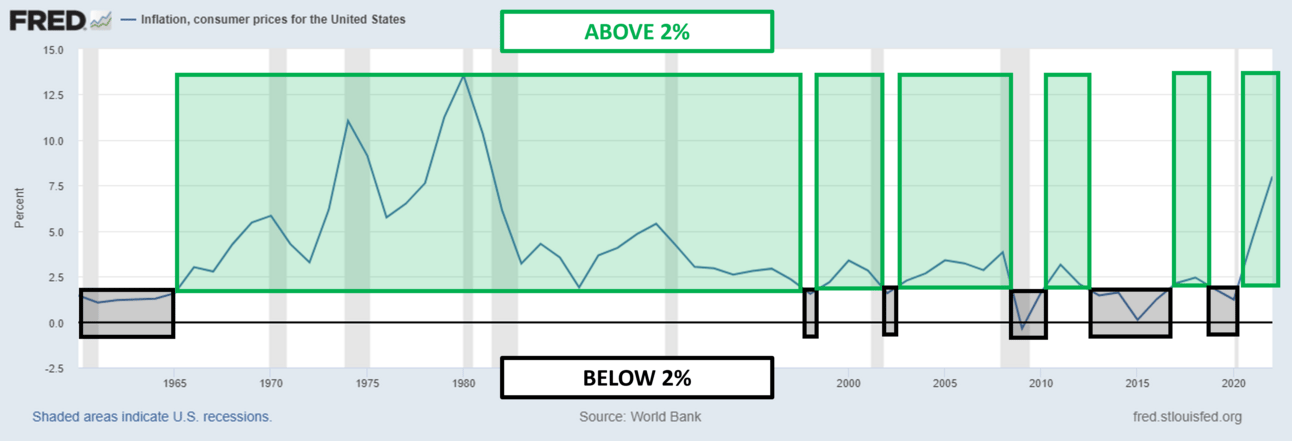

What about the other part of its mandate, inflation?

Chairman Powell said inflation is more important than employment. Economists claim inflation and unemployment have a negative, inverse relationship. In other words, they always move in different directions.

If that’s correct, and employment numbers rarely hit the mark, you’d expect inflation to win most of the time, right? Isn’t that the trade-off?

I guess not. Inflation stayed above 2% in 46 out of the last 63 years.

The Fed whiffed on employment 82% of the time and missed on inflation 73% of the time.

Just you, me, and the markets

Does that mean the US economy is doomed because the Fed almost never hits its targets?

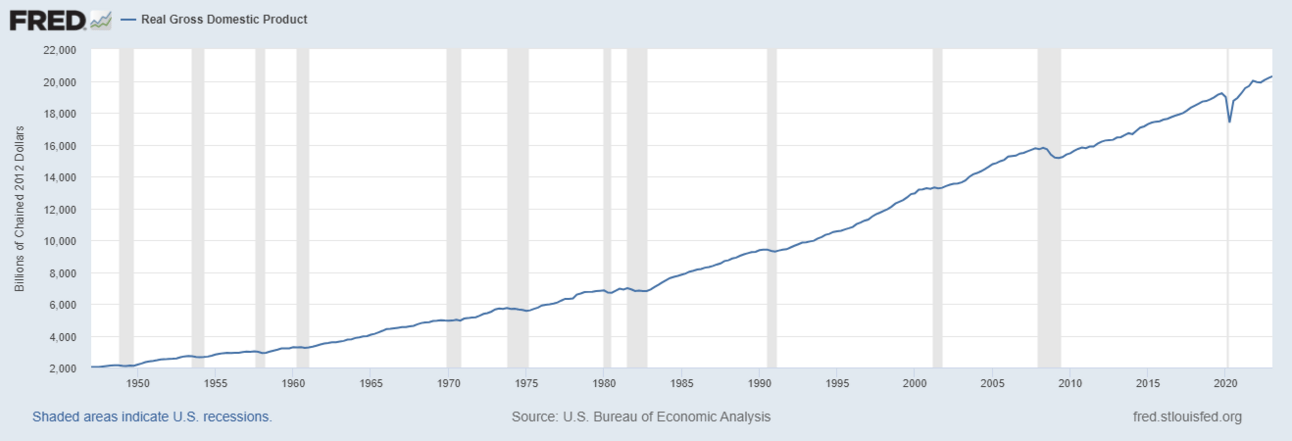

Nope. The US economy has grown in 286 of the past 306 quarters.

More than 93% of the time, the US economy is growing. Asset prices generally go up, too.

The US stock market finishes positive three out of every four years. Real estate has an even better success rate. The price of “stuff” keeps going up, too, regardless of what the Fed does.

The money supply shrinks and grows. Rates rise and fall.

Markets persist.

If you don’t like the results, change them

We may not need to think too hard about this. Central bankers admit they don’t always know the consequences of their decisions. The Chairman of the US Federal Reserve, Jay Powell, said as much. They’re just trying their best.

Usually, that’s good enough.

If not, the government can simply change its benchmarks.

In 2020, the US changed its definition of recession. This year, it changed the way it calibrates CPI, the so-called “headline inflation.”

Next year, it could pick a new definition of full employment or change the inflation target. Maybe it should!

If you move inflation to a 3% target, the Fed hits its mark 31 out of 64 years—a near 50% success rate.

If you bump up the definition of full employment to 5%, then the US economy is at full employment 38% of the time (341 out of 908 quarters).

This is how you solve problems in the legacy system: find a new definition of success or make up your own.

Sadly, my college ECON professors never gave me the same leeway.

New economy, new economics

When I studied economics, we were taught that recessions happen when aggregate production exceeds aggregate demand.

In other words, they come when economies create more things than people can afford to buy, not because the central bank replaced $1 trillion in bank lending with $1 trillion in direct payments to bondholders.

Now, recessions come and go at the will of the Fed. They are no longer a symptom of markets rebalancing and eliminating natural excesses, but rather a product of financial engineering or policy decisions.

The Fed uses many programs to support the US financial system. Open market operations, repo, reverse repo, the discount window, swap lines, and a bunch of pandemic-era lending facilities (most of those are now closed).

Some of these programs are beyond my comprehension, but they are all part of an elaborate system that’s developed over decades.

“Plumbing,” as the experts call it.

I’m not a plumber or an expert, but if I had to guess, all these programs conspire to make interest rates less important. When money is a meme and the system is manipulated at will, the federal funds rate might not have as much importance as we used to think.

Rainmakers

Imagine you and I went outside on a warm, sunny day. After extensive discussion and research, we reckoned that if we jumped up and down and chanted songs, we could bring the rain.

We did it and got no rain.

Undeterred, we did it again the next day. Again, we got no rain.

On the third day, we did it again—and it rained.

Validation!

From that moment on, whenever we wanted rain, we danced and shouted.

Sometimes, it rained that very day. Other times, it would take a good week or more before we got any rain.

We figured that’s normal—rain dances have a long and variable lag.

To get more precise in our rain-making ability, we charted weather patterns and constructed some meteorological theories. It turned out our dancing was more effective on cloudy days. If we started immediately after hearing thunder, we had an almost perfect success rate.

We also discovered some seasonal correlations from one year to the next.

For planning purposes, we put together dot plots and projections based on a Dance Productivity Index, or DPI, as well as surveys and other metrics. People tweeted these things out and started planning picnics around our dances.

As long as we danced every day, we eventually got rain.

They will use data to deceive you

Why do people think our dot plots were nonsense but the Fed’s dot plots are vital data? Why do the CPI charts matter more than our DPI charts?

I can tell you why.

Because centuries of empirical meteorological study proved that dancing does not cause rain.

Economics has no such certainty. As a result, you have to take a leap of faith.

That faith is vital. Without it, the Fed is simply a backstop for the US banking system and a mechanism for incentivizing or disincentivizing debt—not an entity that can achieve maximum employment and stable prices.

Like rain from the heavens

Rain is a natural phenomenon that we can anticipate with some certainty when experts see a confluence of factors but with not enough precision to account for changes in circumstances and the vagaries of climate, wind, and geography.

We can plan for rain. We can make umbrellas, huts, shelter, water-resistant clothes, and all sorts of other things that protect us from the rain. We can find productive uses for rain and change our behaviors to make the most of the times when it rains.

We can’t make it rain, no matter how much we dance.

Is it so much different with the Fed and the US economy?

Maybe when the Fed members say “long and variable lag,” they mean “we don’t know when or how our actions will change anything.”

After centuries of economic research, our financial elites can’t run monetary systems with enough precision to give us the results they expect. The Fed’s own chairman admits this plainly, openly, and nobody seems to believe him.

But I believe him.

Maybe it’s time you should, too?

This post is also available as a collectible NFT on Mirror.

Mark Helfman publishes the Crypto is Easy newsletter. He is also the author of three books and a top Bitcoin writer on Medium and Hacker Noon. Learn more about him in his bio and connect with him on Superpeer or Tealfeed.